Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

QUARTERLY REPORTS Q3 2023

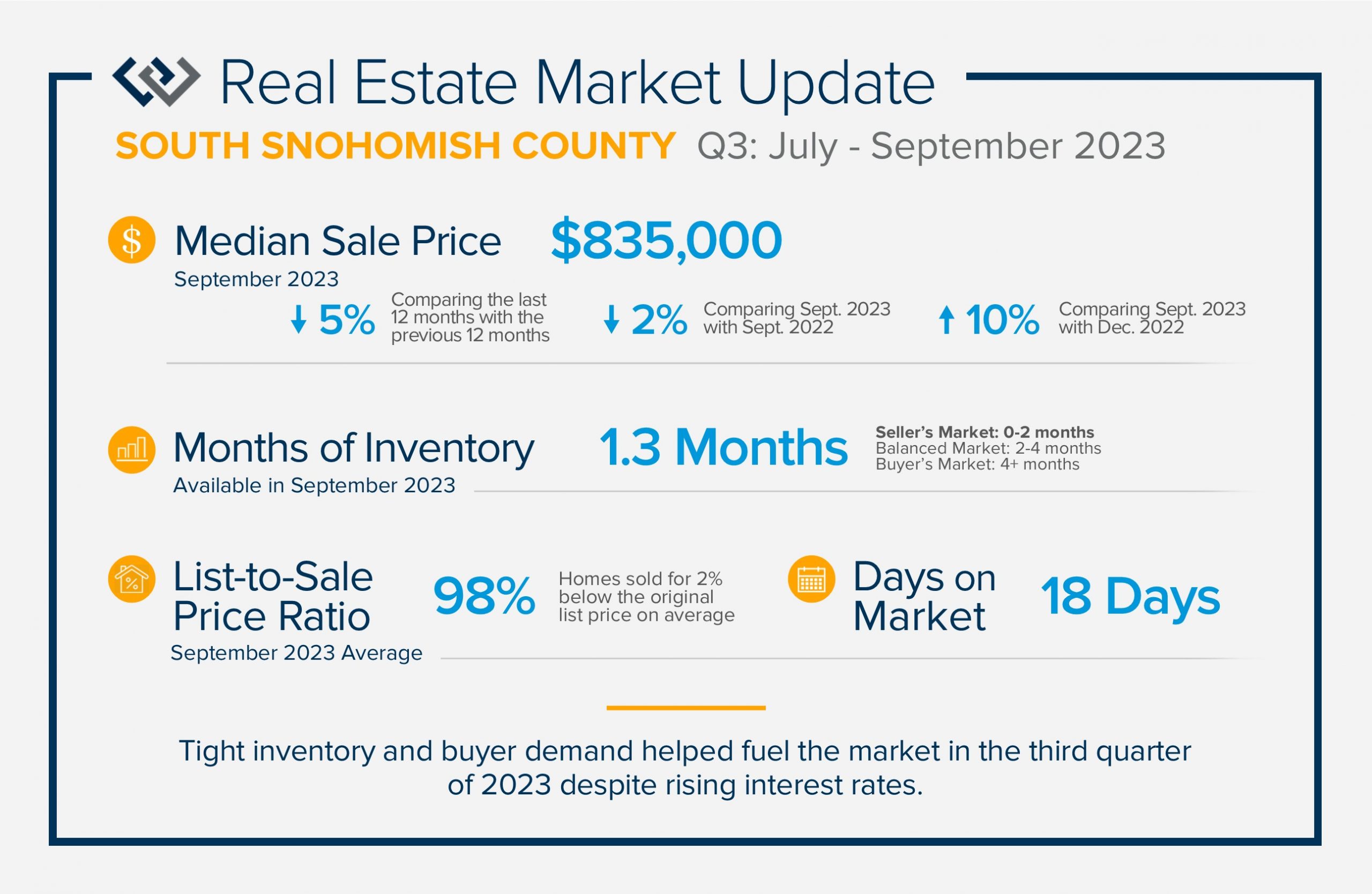

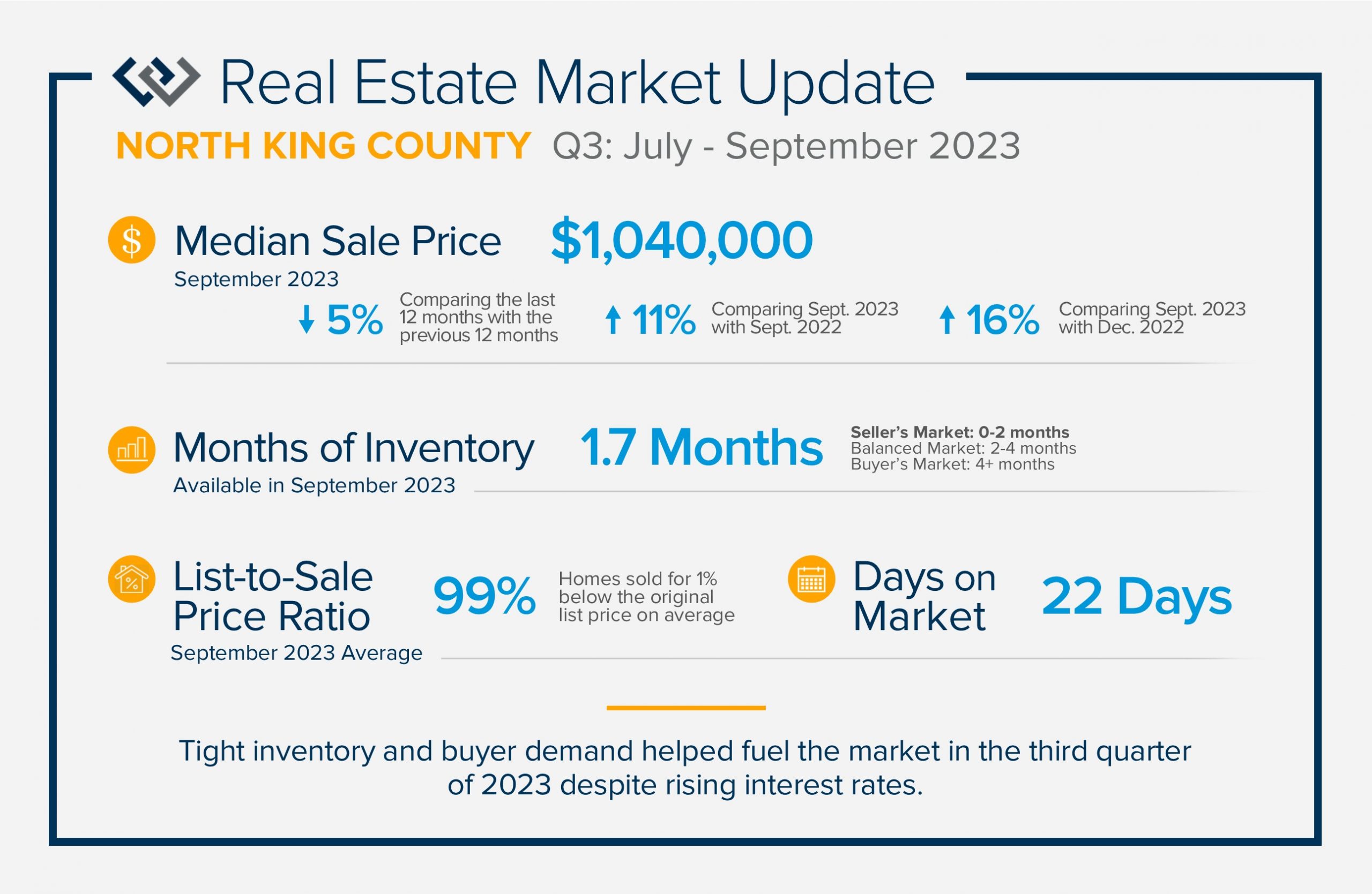

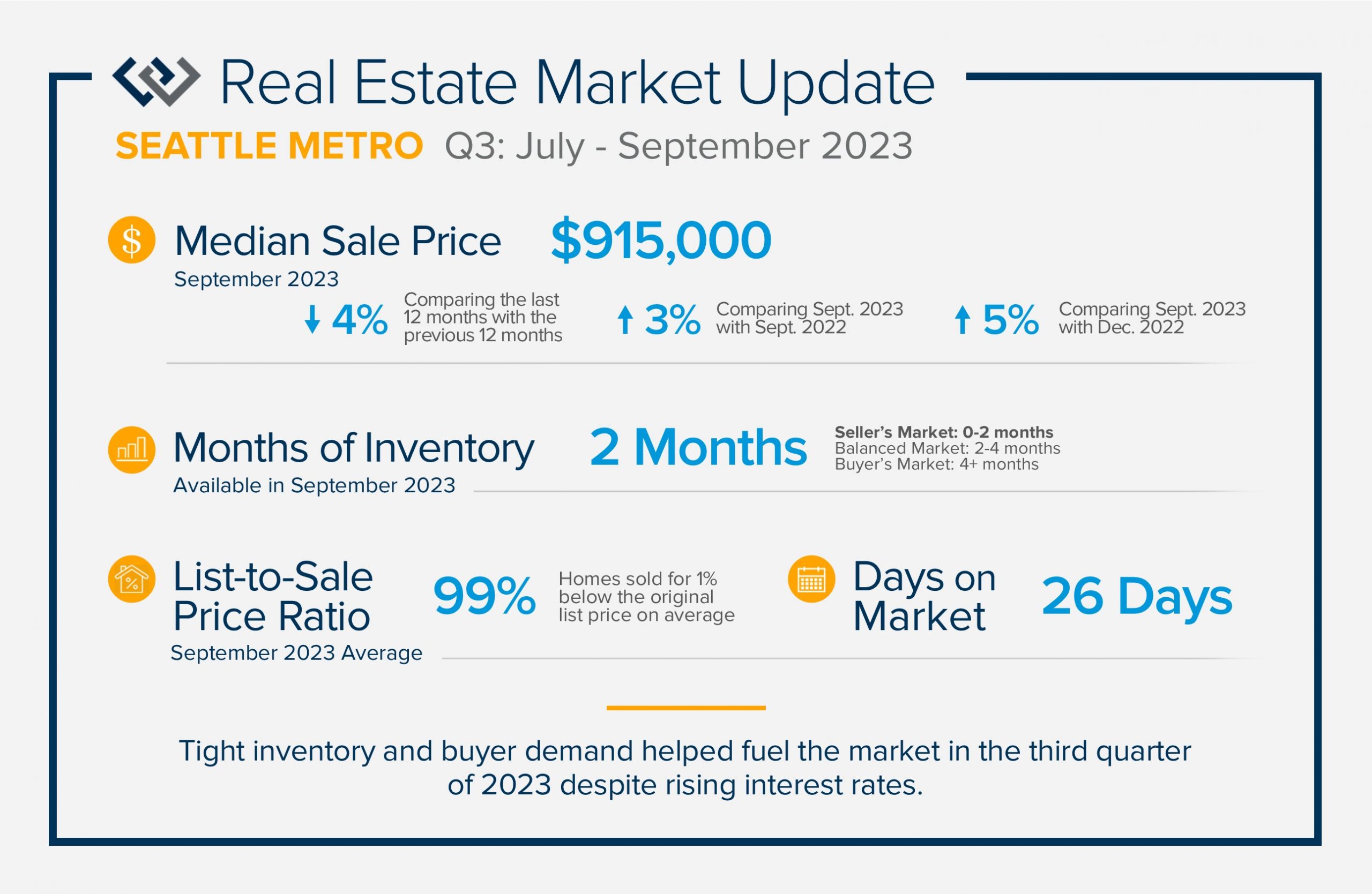

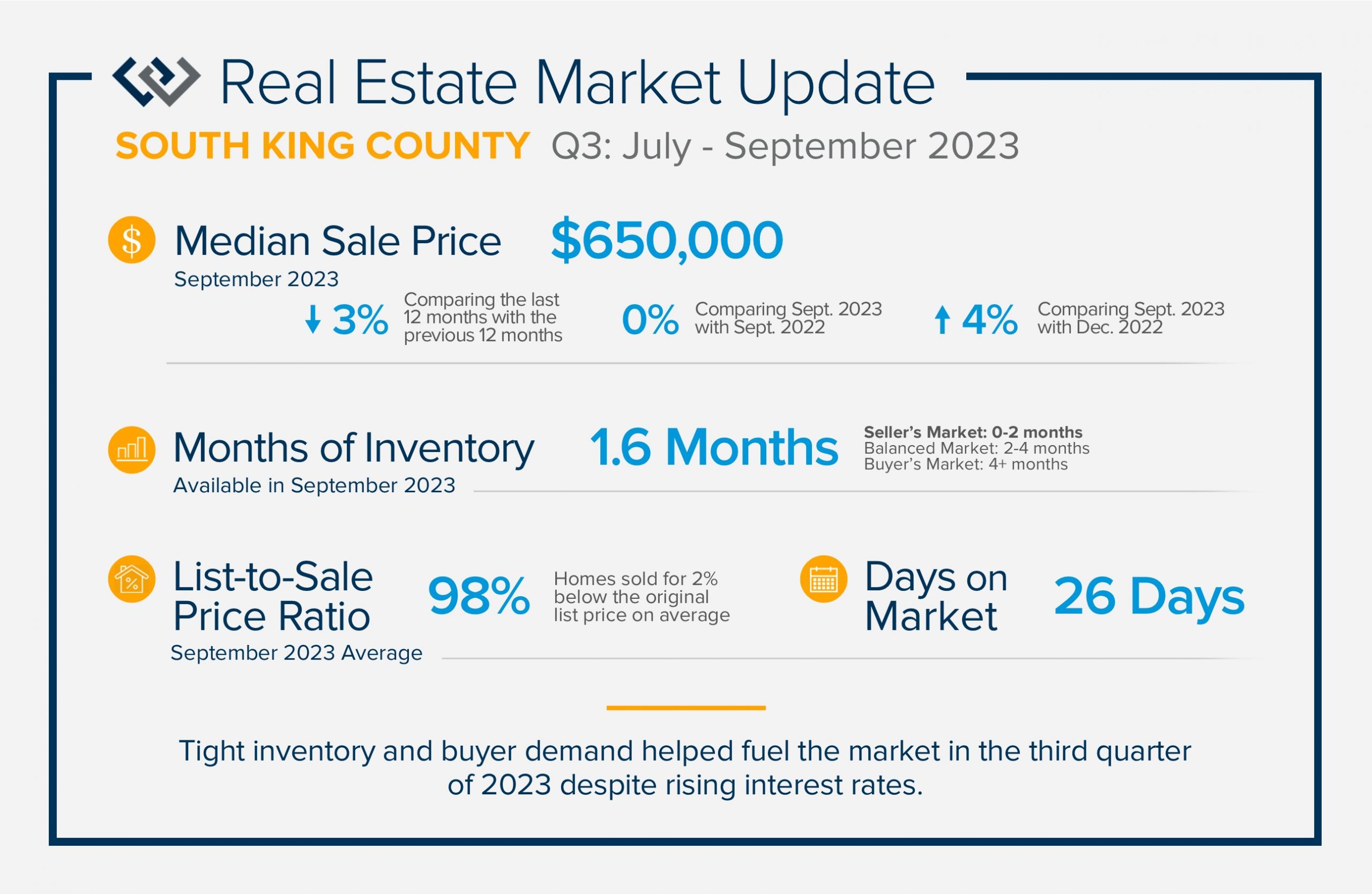

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

Tight inventory and buyer demand helped fuel the market in the third quarter of 2023 despite rising interest rates. There have been fewer listings in 2023 than in 2022 which has created price growth since the first of the year. Prices peaked in spring 2022, corrected in the second half of 2022, and then they started to rise again in 2023. Home equity is high with over 50% of all homeowners having 50% or more equity in their homes.

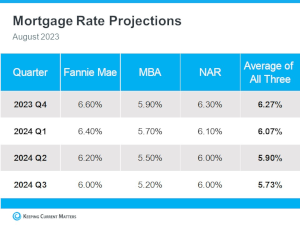

Higher interest rates have been a factor that buyers are having to manage. Some buyers are getting creative with interest rate buy-downs to help ease their monthly payments. Experts predict that rates will decrease over the next 18 months making temporary rate buy-downs attractive.

As we finish out 2023, we anticipate inventory to remain tight and buyer demand to continue. Sellers who are deciding to cash in their equity now are finding success. If you are curious about how the real estate market relates to your goals, please reach out. It is my goal to help keep my clients informed and empower strong decisions.

The Low Inventory Effect: Nationally & Close to Home

The video below from Matthew Gardner, Windermere’s Chief Economist, refers to the effects of constricted inventory levels on the national housing market in a higher interest rate environment. Review the localized numbers that I gathered that pertain to King and Snohomish Counties and then check out what he has to say about the national trends.

Overall, inventory has been tight in 2023! Many people made moves in the pandemic-fueled market and are deciding to stay put. They utilized the lower interest rates to secure their long-term home and don’t see a need to move anytime soon. Did you know the average person stays in their home for 10 years?

Others are not completely satisfied with their homes but feel attached to the lower rate and are pushing through the discomfort until rates settle. Some are deciding to come to market because their homes do not fit their lives anymore and some are bucking the rates and getting creative with financing. The buyers working the creative financing route with rate buy-downs will be rewarded when rates lower and prices go up.

Year-to-date new listings in King County are down 30% over 2022 and down 37% in Snohomish County. Closed sales are down 27% over 2022 in King County and down 27% in Snohomish County. Even though there have been fewer new listings year-over-year, the closed sale percentage is tracking more favorably which demonstrates buyer demand. This is why inventory is tight. In August 2023 there were 1.3 months of inventory in King County and 1.1 months in Snohomish County. This illustrates a seller’s market.

Closed sales peaked in 2021 in both counties at 20,132 in King County and 8,663 in Snohomish County. As we venture away from these outlier pandemic years, consumers are wrapping their heads around the changing environment. Year-to-date, King County has had 16,069 closed sales and 5,344 in Snohomish County. Year-to-date, King County is pacing slightly higher than 2019, which was a normal market prior to the pandemic and Snohomish County is lagging behind by just a bit.

The pace of inventory has helped stabilize prices and created price growth since the start of 2023. Buyer demand exists because people’s lives change and we have the Millennial generation out in full force. If your life is leading you to consider a move, please reach out. Please do not rely on the noise in the media, they will lead you astray.

I can help you dig into the data and devise a plan that relates to YOUR life. With equity levels astoundingly high (over 50% of homeowners in the U.S. have over 50% equity), moves are being made with great success. For buyers, the rates can be overcome with some creativity, lived with for now, or you can set a benchmark for when you’re ready. If you are curious about how today’s market relates to your goals or want to make a plan for the future, let’s talk! It is always my goal to help keep my clients informed and empower strong decisions.

Were you like me and turned the heat on when the rain came this week? It’s that time of year when our heating systems need to be attended to, to be properly prepared for the colder months ahead.

Have your air and ventilation systems inspected by the professionals to ensure efficient and healthy airflow. This will also ensure that your systems are running safely and lower your risk of fire. Note: if you need to purchase or replace any major household appliances, September and October are usually when the latest models are revealed.

Win-Win: How to Overcome Interest Rate Pressure with Creative Financing

Lately we have talked about life changes leading to real estate moves. Sometimes moves are brought on by joyful advancements in life and sometimes they are motivated by hardship. Then there are times when your actual house just doesn’t fit your life anymore and it is time for something different. Whatever might be calling someone to make a move, they also have to assess the affordability.

There are three aspects to affordability: price, interest rate, and income. Price and interest rate will determine your monthly payment, and your income will provide the means to maintain and build your investment. One way I have been able to help my clients strategize affordability with higher interest rates are some creative financing options.

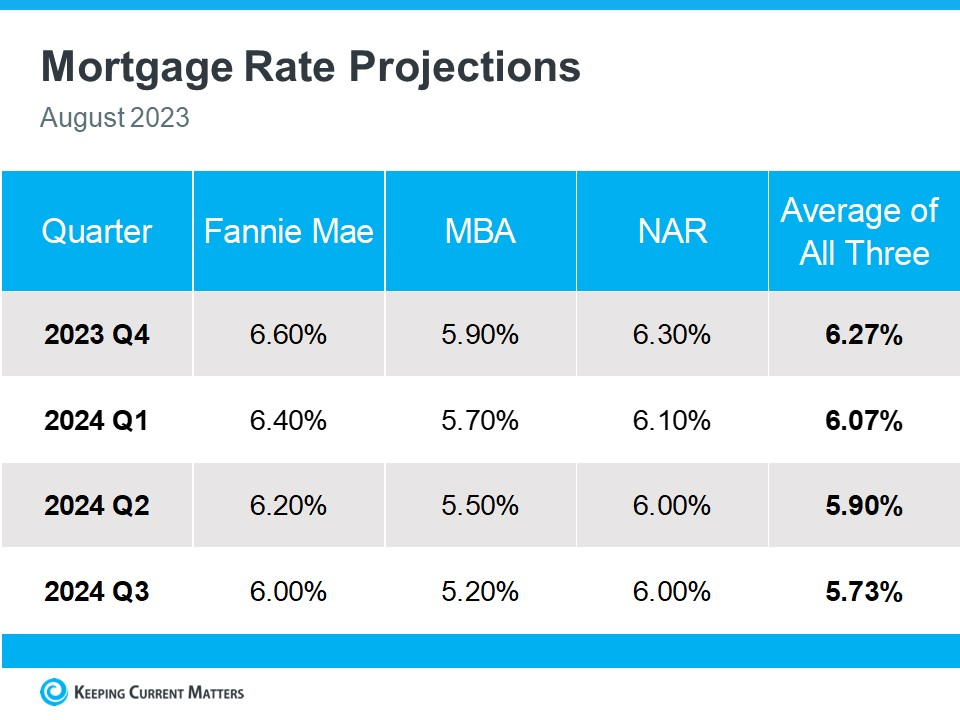

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

I have helped some of my clients overcome the higher interest rates and secure today’s prices by helping them arrange with their lender an interest rate buy-down. Sometimes we have even been able to get the seller to financially assist in paying for the buy-down. There are two types of buy-downs: a permanent buy-down and a temporary buy-down.

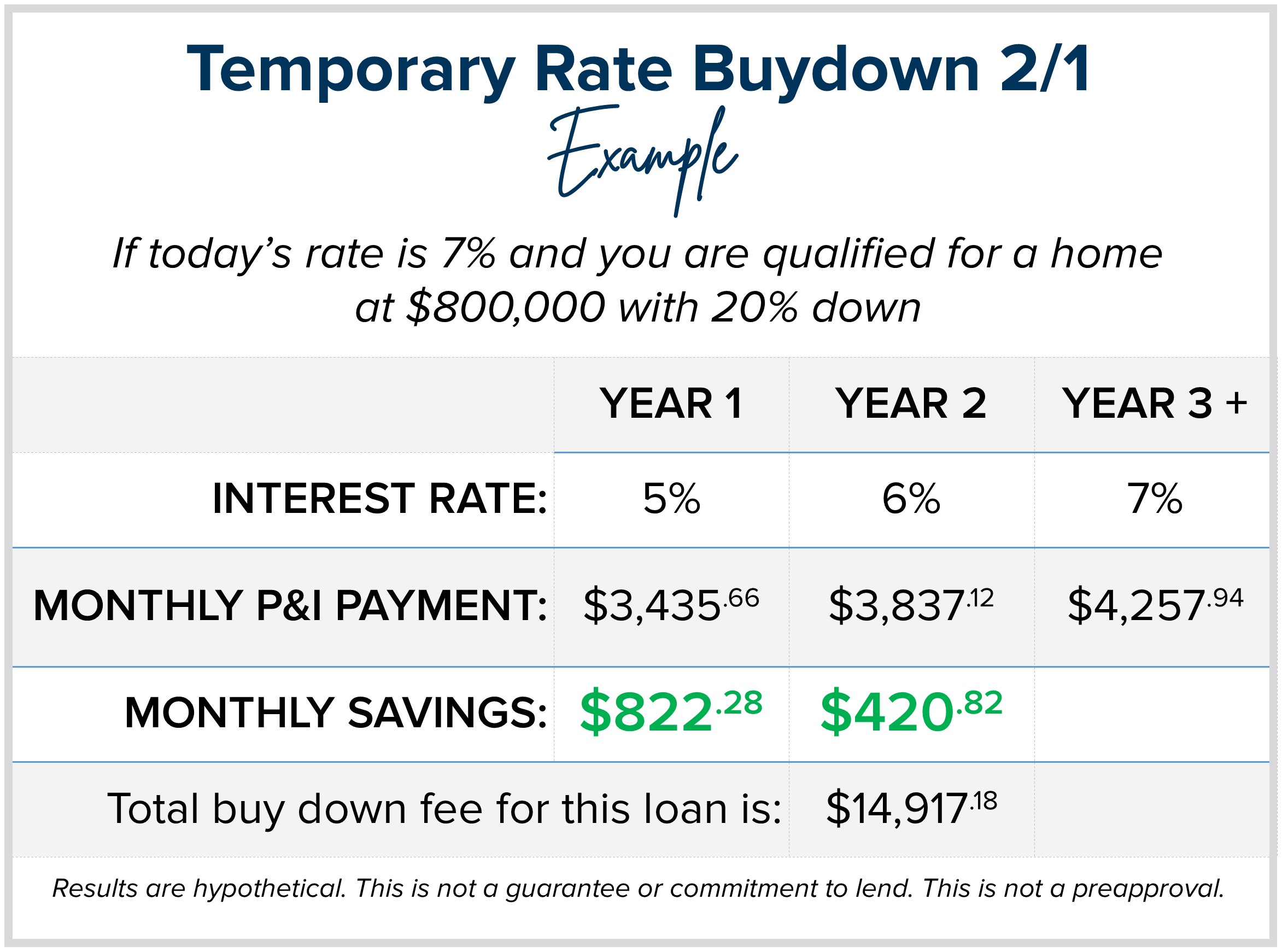

A permanent buy-down requires about 3% of the purchase price to buy the rate down by a point for the 30-year term of the loan. A good rule of thumb to remember is that every 1-point in rate equals 10% in buying power. For example, if the rate is 7% and you are qualified for a home at $800,000, if the rate went down by 1 point to 6% you could now afford $880,000 and have a very similar payment. Another way to look at this is simply the monthly payment itself. An $800,000 purchase with 20% down with a 6% interest rate would save a buyer $420.82 a month vs. the payment at 7%.

A permanent buy-down is a useful tool and so is a temporary buy-down. It is actually one of the most powerful tools in today’s market. It costs far less than a permanent buy-down and with rates predicted to decrease over the next 12-18 months as inflation settles, you could easily find yourself in a position to refinance.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

The roughly $15,000 in monthly payment savings is paid upfront at closing and in some cases paid by the seller. The buyer still needs to qualify based on the 7% interest rate as the payments will convert to the payment based on the 7% in year three moving forward. The strategy here is to never have the payment increase to 7% amount because the buyer plans to refinance when rates come down and will permanently fix their rate below 7%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases those funds can be applied towards the refinance.

This strategy has been effective in helping buyers secure a monthly payment that is more affordable so they can make a move now based on life’s needs and wants. It also helps them secure today’s prices. If we find a home that has had a little longer market time, a home seller is likely to assist with the $15,000 credit vs. reducing their price by 3% to accommodate a lower payment for 30 years. The temporary assistance in reducing the payment for 1 to 2 years is a viable tool for both the buyer and seller to create a win-win.

I felt it was important to bring these options to light and to encourage people to not just take today’s market at face value. Creativity, collaboration, and calm have led to some of the most rewarding sales this year for both buyers and sellers. When people logically work together to accomplish moves in an environment that seems difficult, they find success. Ultimately, I am here to help my clients match their real estate to their lives despite where the rates are today.

I love rolling up my sleeves and creating a plan to help my buyers and sellers accomplish their goals. It is my mission to help keep my clients informed and empower strong decisions. If you or someone you know are curious about how today’s market matches your needs, please reach out.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you!

Should You Stay or Should You Go? Interest Rates Limit Inventory and Stabilize Prices

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control.

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control.

While there was a correction from May 2022 to January 2023, since then prices have started to grow again despite the rates hovering in the 6-7% range. In fact, the median price is up from the bottom (Jan/Feb 2023) by 13% in King County and 9% in Snohomish County. Further, the median price in July 2023 was even with July 2022 in King County and down by only 2% in Snohomish County. This is a sign of price stabilization. Historically, the impact rising rates have on prices year-over-year is not negative. We are in the midst of proving that same theory.

Believe it or not, the higher rates are keeping prices stable because it is limiting the available inventory for sale. You see, there are plenty of buyers out looking for homes right now, and inventory levels are tight because potential sellers are waiting to make a move because they are holding on to their low rate. Our job market is good, we have people moving to our area and the millennials are out in full force searching for their first homes.

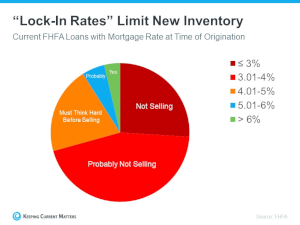

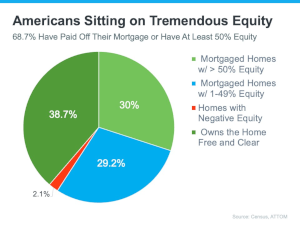

There are two interesting phenomena going on with potential home sellers right now. First, according to ATTOM Data, 68.7% of homeowners have at least 50% equity and only 2.1% have negative equity. This is the number one indicator that we are not in a housing crisis or bubble. Second, according to FHFA, 70% of homeowners with a mortgage have a rate 4% or lower. This is causing people who are no longer happy with where they live to stay a bit longer because they don’t want to give up their payment just yet.

Here’s the deal though, housing is a reflection of life! According to the US Census, 66% of homeowners would like to upgrade to a nicer home with features that better match their lifestyle, and 45% would like to move to a home to better match the changing size of their household. Life changes motivate moves! Many people are waiting out these life changes until rates come down so they can better afford their desired transition. This has put downward pressure on inventory, limiting selection for buyers, hence creating price growth and stabilization.

Here’s the deal though, housing is a reflection of life! According to the US Census, 66% of homeowners would like to upgrade to a nicer home with features that better match their lifestyle, and 45% would like to move to a home to better match the changing size of their household. Life changes motivate moves! Many people are waiting out these life changes until rates come down so they can better afford their desired transition. This has put downward pressure on inventory, limiting selection for buyers, hence creating price growth and stabilization.

So, what is going to happen when rates come down? Experts across the board predict that rates will recede as inflation gains control. This will be a gradual process over the next 12-18 months. The biggest indicator will be inflation reaching the 2% year-over-year mark. Once we hit this point, which we are close to, experts predict the Fed will be comfortable easing off the higher rates. This will cause more homes to come to market as the delta between the rate a homeowner currently holds and what they are willing to take on to indulge their desire to move, will become more attainable. Plus, as rates recede it will increase buyer demand.

We find ourselves in a delicate dance with inflation, rates, inventory, and prices. Someone who desires a move has to consider the impact the rates can have on their payment. Many of these buyers are taking the leap and finding creative ways to offset the rate such as ARM financing, rate buy downs, or they are preparing to re-finance their purchase when rates come down. This way they will have secured a good price which is the basis of their loan.

We find ourselves in a delicate dance with inflation, rates, inventory, and prices. Someone who desires a move has to consider the impact the rates can have on their payment. Many of these buyers are taking the leap and finding creative ways to offset the rate such as ARM financing, rate buy downs, or they are preparing to re-finance their purchase when rates come down. This way they will have secured a good price which is the basis of their loan.

So, do you stay or do you go? According, to the lyrics from the classic song from The Clash, “if I stay there will be trouble, but if I go there will be double.” This is up to you to decide. Where I can help is to gather the data and help you analyze the market in order to empower you to make the best choice for you and your family. For some, the right time is now and for others, waiting a bit longer will be a good plan.

What I do know, is that when we hit the inflation rate that the Fed is comfortable with and they ease off of rates, the market will tilt. This will be a benefit for some and a challenge for others. In other words, there is not one right answer for everyone and that is where I think I have the opportunity to serve my clients best.

Helping people navigate the ever-changing market is a skill, an art, and a calling. I am here for it and find great satisfaction in helping people make big life decisions that help bring joy, solve problems, and make them money! My job is a huge responsibility and it is an honor to serve my clients. If you or someone you know are wondering about how today’s market conditions affect your goals, please reach out. We can dig into the data, assess your dreams and devise a plan.

Helping people navigate the ever-changing market is a skill, an art, and a calling. I am here for it and find great satisfaction in helping people make big life decisions that help bring joy, solve problems, and make them money! My job is a huge responsibility and it is an honor to serve my clients. If you or someone you know are wondering about how today’s market conditions affect your goals, please reach out. We can dig into the data, assess your dreams and devise a plan.

Clarity Through Chaos: Using the Data to Guide Decisions.

I think we can all agree that we have been on a bit of a wild ride over the last 12 months in the real estate market. When the Fed decided to change its trajectory on interest rates in mid-2022, it created some chaos and confusion.

When big changes happen, it is a natural reaction to pause and wait for some certainty of how things will land. This happened when the pandemic hit, too. People paused in March and April of 2020 and once May settled in the market went bonkers. I have found that gathering data, whether it’s real-time data or studying historical trends, in order to make sense of it all is incredibly helpful to create clarity and empower strong decisions.

I am committed to studying the data on behalf of my clients and I am also fortunate to have Matthew Gardner, Windermere’s Chief Economist as a source to help guide this research. He speaks to the predictions that were made at the beginning of this year by several industry experts and breaks down their varied theories in this recent article. As a testament to the importance of gathering the data and applying knowledgeable analysis are the now renewed predictions from all of these sources. They are now very much more aligned with one another and in agreement that prices are not headed in a downward spiral, but are in fact on the rise year-over-year. Data is powerful!

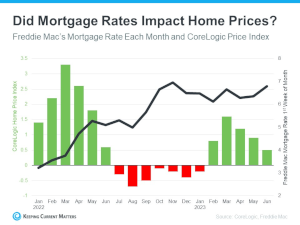

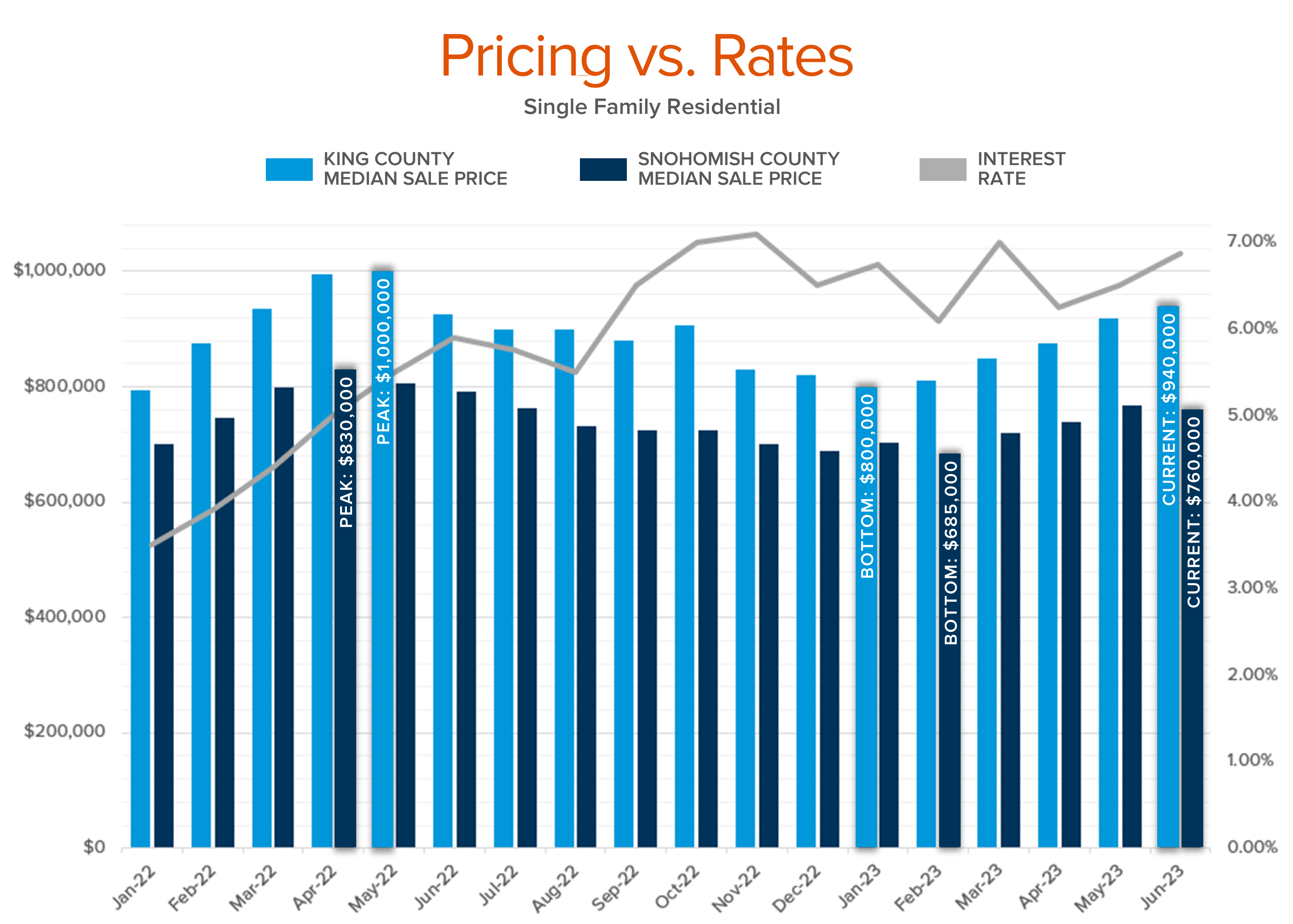

Below is a chart I created with hyper-local data reflecting both King and Snohomish counties’ median prices over the last 18 months in relationship to the rising interest rates. While we are off the peak of 2022 when rates were at 5%, we are only slightly lower and up quite significantly from the bottom when rates hit 7%. Proof that the market is sustaining the higher rates is that we have found ourselves back near the 7% this summer and prices have not faltered.

Would the market welcome a drop in the rate? Absolutely! When this happens, which is predicted, we will see buyer demand increase. What we will also see is additional inventory come to market as would-be home sellers will be more comfortable relinquishing their low rate to indulge their need or want for a different home. The high rates are keeping inventory low in a high-rate environment, which is supporting price stabilization and growth. Simply put, the sky is not falling.

The market continues to churn, we are not in a free fall, and prices are stable. If you’ve thought about a move, consider the data and please ask me to help you gain understanding. I can adjust the graph featured here with your local zip code or city to give you an even more thorough look at your investment.

Real estate moves are most often a result of life changes. If you have found yourself questioning whether your four walls currently meet your needs, let’s talk! I will assess your goals and apply the data in an understandable way to help guide the best decision for you today or down the road.

The need for food assistance has never been greater due to the end of the Supplemental Nutrition Assistance Program’s (SNAP) Emergency Allotments and soaring food prices. As a result, more and more families across America are facing hunger. Our food banks are experiencing a surge in visitors and struggling to meet the increased demand.

The good news is that this incredible network of go-givers can do something about it!

Fueled by the collective generosity that Windermere is so well known for, I’m rallying my network to come together to help us towards our goal of raising $50,000.

I would be very grateful if you considered contributing to our campaign through our donation website.

Thank you for your generosity!

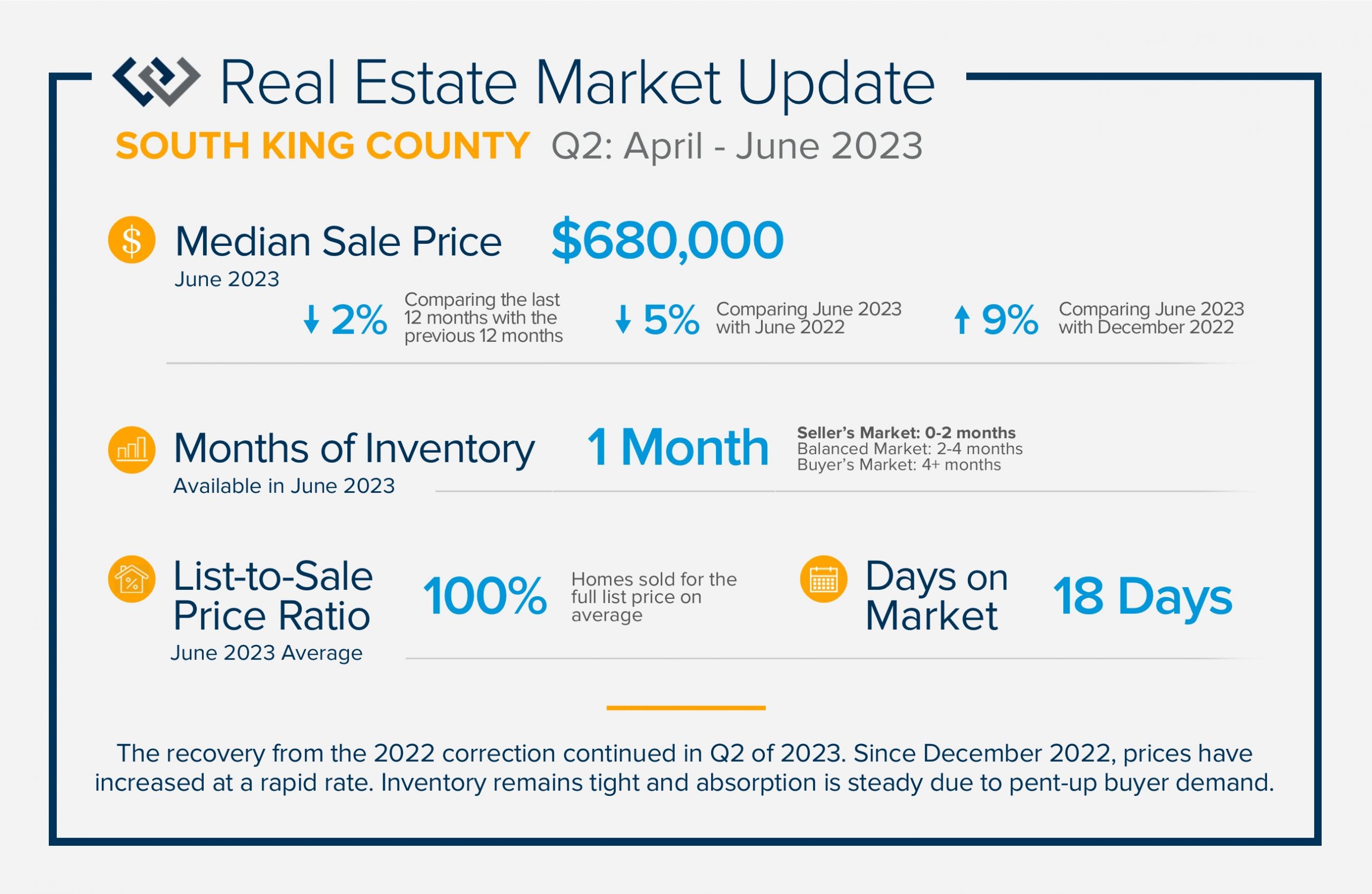

QUARTERLY REPORTS Q2 2023

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

If you are curious about how the trends relate to your goals, please reach out. It is my goal to keep my clients well-informed to empower strong decisions.

2023 Market Predictions, Fact Checked.

One of the reasons why we are fortunate to have Matthew Gardener as our Chief Economist at Windermere is his transparency. Every year, Matthew makes predictions for the coming year based on his monumental research and years of experience. Just this week, he reviewed his 2023 predictions and recorded the video below. Most of his predictions were spot on and only two were slightly off. That is pretty good considering crystal balls don’t exist.

In the video recap below, he covers the trajectory of home prices, interest rates, inventory levels, the shift of the work-from-home trend, zoning changes, and affordability. All of these factors play into people making informed decisions about their real estate. He is certainly an asset that I can rely upon to help me guide my clients.

Overall, it is important to note that prices are heading in a positive direction, interest rates may take a bit longer to settle and inventory remains tight. I am seeing buyer demand return to the market and prices have grown since the first of the year.

He also mentions that real estate is local and that trends can vary by location. That is where I can help you. I am deeply invested in understanding the market in the communities and neighborhoods that surround us. If you are curious about how the trends relate to your real estate goals, please reach out. It is always my goal to help keep my clients informed and empower strong decisions.

Windermere Community Service Day

Windermere Community Service Day

This is the 8th year that my office has spent our Community Service Day working to put fresh produce on the tables of local families who need a little help. We work with the Snohomish Garden Club, planting over a half-acre of veggies and fruits that will be harvested into thousands of pounds of fresh produce over the summer and into the fall.

If you’d like to pitch in, you can donate to our Summer Food Drive, or bring donations to my office, through August 4th. All donations will go to Volunteers of America Western WA food banks.

Since 1984, Windermere associates have dedicated a day of work to complete neighborhood improvement projects as part of Windermere’s Community Service Day. After all, real estate is rooted in our communities. And an investment in our neighborhoods gives us all a better place to call home.

Let’s Dance! Prices Stabilize & Even Grow Amidst a Chaotic Interest Rate Market

If we let the media determine the mood regarding the housing market, it would be time to shut the party down and call it a night. I’m here to report that we are still dancing and there is a lot to celebrate! While it is not all shiny and bright (it never is), there is a pattern of consistent growth and the sky is far from falling. The environment has changed from a year ago and we are still moving to the beat of the drum despite some rain (insert dancing emoji here).

The latest headline from the Seattle Times claims that prices have tumbled from last year. While prices are down from a year ago the story is much more detailed and it is far from a tumble. The DJ (The Fed) played some songs (hiked rates) that cleared the dancefloor for a bit, but the hits are playing now and demand is strong! The headline I have included above is a much more accurate depiction of the pricing journey over the last year and a half, and it is actually pretty great.

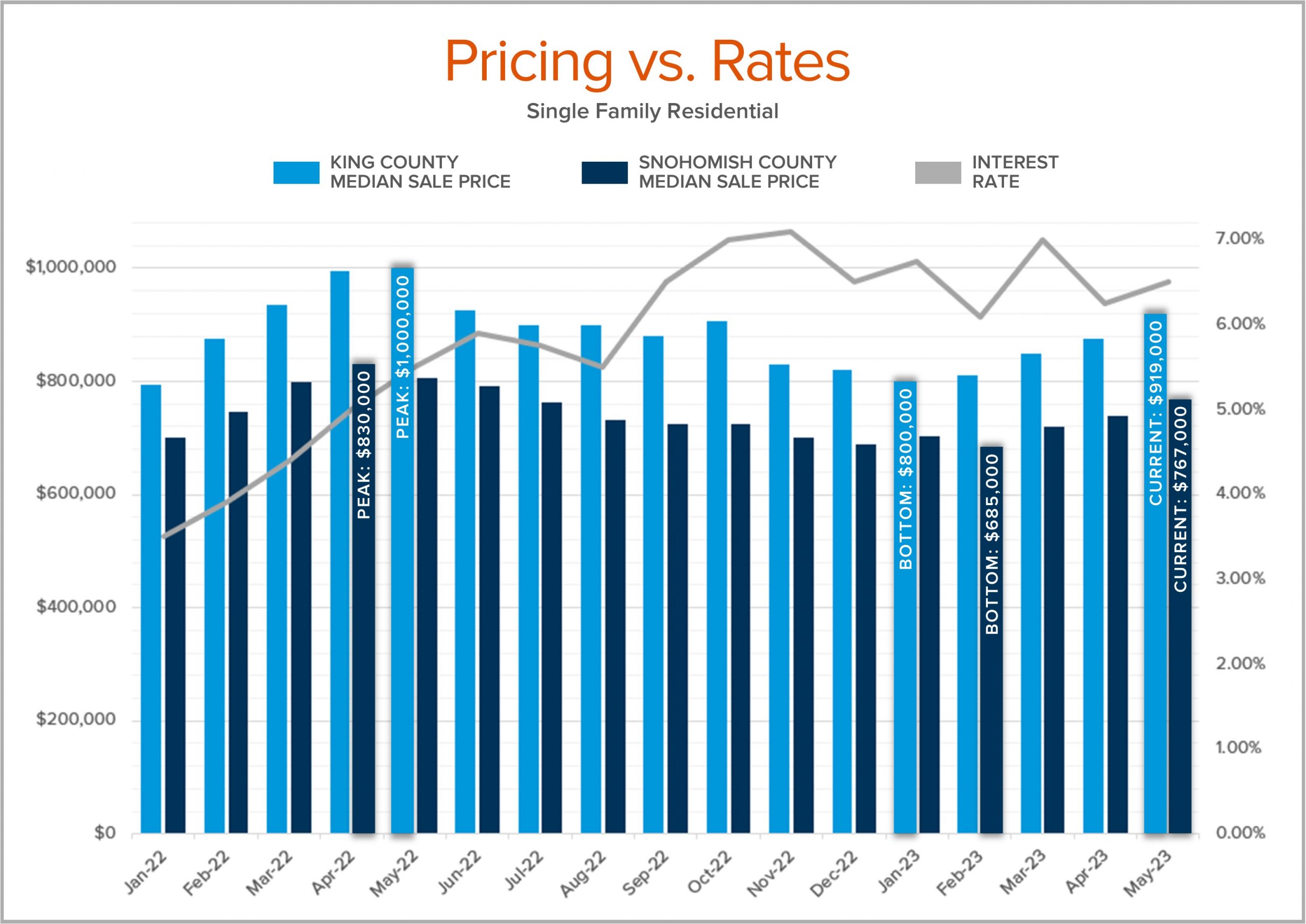

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In Snohomish County, the median price peaked in April 2022 at $830,000 and is currently at $767,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in February 2023 at $685,000 which was down 17% (the actual tumble) from the peak but are now up 12% from the bottom!

This was a relatively quick correction that is trending in a positive direction as the market gets used to higher interest rates. Quantitative Easing could not last forever and rates had to go up to combat inflation. During the same time frame detailed above, interest rates dramatically changed.

In May 2022, they averaged 5.5% (the peak) and in January 2023 they averaged 6.75% (the bottom). In fact, they started 2022 at 3.5%, a level we will likely never see again! Currently, rates are hovering in the high 6% and are predicted to slowly recede as we enter the second half of 2023. Proof that buyers have become conditioned to the new normal of rates is that prices have grown from the start of 2023 (January – May 2023): 14% in King County and 11% in Snohomish County, despite rates remaining in the 6% and at times cresting 7%. When they go down to the lower 6% or even the high 5%, expect prices to climb at a faster rate. Will there be a buyer mosh pit? Buyers should be weighing these effects as they choose when to act. Rates can always be re-financed, but the sale price cannot.

While the homeowners that purchased during those peak months have some time before they regain their home’s value, it will happen. We are a year out from the peak and the last time we had a correction in 2018 it took 17 months to recover. That subsection of sales aside and equity levels are strong. Imagine the hope you feel when watching the first dance at a wedding to the classic It’s A Wonderful World; the party is just getting started. Prices are up in King County by 27% from March 2019 to March 2023 and in Snohomish County up 46%. Ten-year gains are astounding at 140% in King County and 179 % in Snohomish County.

This leads me to my biggest takeaway; real estate moves are dictated by life changes. Maybe the DJ plays Sweet Home Alabama and you rush to the dance floor because it’s time to move closer to family, or Marry You inspires you to take the plunge into married life as you spin the night towards household formation. My point is, change drives demand.

While real estate is an investment, it is also where we live. It is our refuge, our security, and our joy. We usher in pleasure and pain in the four walls we call home and at some point, that will lead to wanting something more, less, or just different out of our home. I understand that these moves may have been put on hold while the DJ figured out the crowd. Currently, the dance floor is becoming more crowded. The attendees at the party are realizing that we only live once and that we are not going back to the discotheque of 3-4% interest rates; they are ready to boogie!

The dancing/party metaphor was a fun way to tell a complicated and emotional story. This correction and recovery have been a bit hard and confusing, especially after the disruption of the pandemic. We are just getting our dancing shoes broken in again. If life has met you at a crossroads of change and you are curious about how real estate relates to this for you, please reach out. I am deeply invested in the data and my service is always rooted in educating my clients. It is my goal to help the people I serve navigate smooth transitions that are financially stable and strong and match their homes to their hearts.

Windermere Community Service Day

Since 1984, Windermere associates have dedicated a day of work to complete neighborhood improvement projects as part of Windermere’s Community Service Day. After all, real estate is rooted in our communities. And an investment in our neighborhoods gives us all a better place to call home.

This Friday, my office will spend the day with the Snohomish Garden Club working to put fresh produce on the tables of local families who need a little help. We will plant over a half-acre of veggies and fruits that will be harvested over the summer and into the fall.

If you’d like to pitch in, you can donate to our Summer Food Drive, or bring donations to my office, through August 4th. All donations will go to Volunteers of America Western WA food banks.

A Busy Legislative Session for Housing: 10 Bills Passed That Will Affect Housing in Our State

On April 23rd the Washington State Legislature adjourned after passing 10 new bills that will affect housing. Some of the bills are geared toward creating more transparency around brokerage transactions, some are intended to institute more opportunities for building density to provide more affordable housing, and some are more regulatory to help guide and ease the permitting process for building and development.

The bills that will improve real estate brokerage services are centered in transparency and cleaning up some laws that do not trend with market conditions. As of January 1, 2024, all real estate brokers will be required to engage in a buyer service agreement with the buyers they work with, similar to the requirement of having a listing agreement with a seller (SB 5191). These service agreements, better known as Buyer Agency Agreements (BAA) will address compensation, exclusivity, the duration of the relationship, and establish written consent for dual agency. This will create clearly defined broker representation for buyers from the onset of the relationship.

Short-term seller rent-backs after closing are now carved out of the landlord-tenant act if the rent-back is less than 90 days (SHB 1070). This will ease the angst involved with tenant rights, as the goal of a rent-back is to create a convenient transitionary period that intends for the seller to vacate, minimizing their tenant rights. This change aligns with the trends in the marketplace and makes this solution-based approach less tenuous. Lifetime listing agreements were also shortened (SSB 5399).

Washington State ranks last in the number of housing units per family nationally and officials project that the state will need roughly one million new homes by 2044. Many of the bills that passed last month will create policies to help provide more housing units and affordability. Matthew Gardner, Windermere’s Chief Economist has been speaking about our state’s lack of affordability for years and shares his thoughts here on the HB 1110 which will allow for the development of middle housing.

HB 1110, SB 5258, HB 1042, and HB 1337 were all created to create more housing units. HB 1110 addresses middle housing, SB 5258 modifies several laws relating to the construction of condos and townhomes, HB 1042 enables the creation of housing in existing, underutilized buildings, and HB 1337 will make it easier to build Accessory Dwelling Units (ADUs) in urban growth areas.

SB 5412, SB 5290, and HB 1293 are intended to ease the permitting and design review processes when applying for a building permit. These should help streamline and accelerate getting from point A to point B on a building project. With the goal of providing more housing units, the backend systems needed to be reevaluated to meet these goals in a timely fashion while adhering to important guidelines and procedures.

Lastly, HB 1474 will increase the document recording fees by $100 to fund a new state program to provide down payment and closing cost assistance to people, or heirs, impacted by racially restrictive covenants. This program is set to raise $75 million per year to improve housing affordability. The State also committed over $1.1 billion in budget funds to work towards investing in housing supply and homelessness prevention.

Click here for a detailed review of each new bill and the budget changes. It is always my goal to help keep my clients well-informed about the real estate market and in this case, knowing the direction our state is headed with the laws surrounding real estate and housing. If you have additional questions or want to discuss how these changes may affect your housing goals, please reach out.

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

Since 1984, Windermere associates have dedicated a day of work to complete neighborhood improvement projects as part of Windermere’s Community Service Day. After all, real estate is rooted in our communities. And an investment in our neighborhoods gives us all a better place to call home.

Our office will spend June 9th with the Snohomish Garden Club working to put fresh produce on the tables of local families who need a little help. We will plant over a half-acre of veggies and fruits that will be harvested over the summer and into the fall.

If you’d like to pitch in, we are looking for additional veggie starts. Let us know if you have some starts already going or if you would like to prepare some now that you would be willing to donate.

The garden specifically needs:

- Scallions

- Snow/Pod Peas (please no shelling peas)

- Chard

- Lettuce (the food banks require headed varieties, rather than loose-leaf)

- Squash (any kind, EXCEPT yellow crookneck)

- Cabbage/Broccoli/Kohlrabi/Cauliflower/Collards/Kale

- Peppers (early maturing varieties work great: ~70-day range)

- Herbs (never enough Basil and Parsley!)

- Flowers (marigolds, nasturtiums, or any annuals)

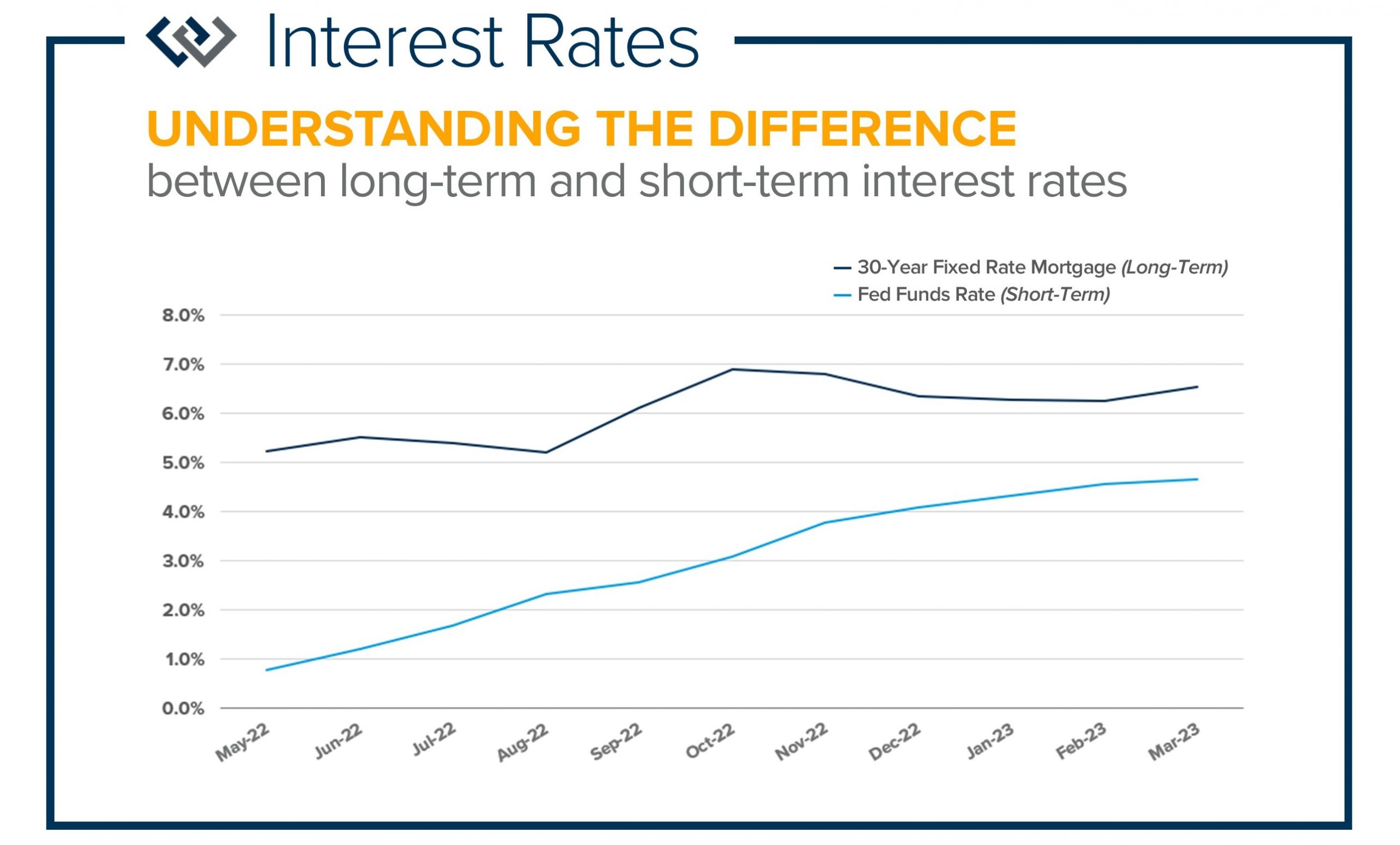

Understanding the Difference Between Long-Term & Short-Term Interest Rates

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

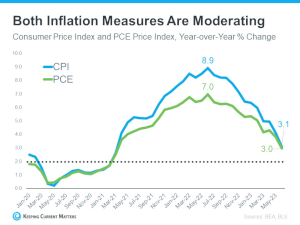

In an effort to combat inflation and slow spending, the Fed has made consistent increases to the short-term rate over the last year. I am sure you are running out of fingers on your hands to count the number of times you have heard this as a top story on the news: “The Fed Raises Rates!”. A huge misconception has been that the rates the Fed are referring to are mortgage rates.

As you can see from the chart above, the short-term rate has had a consistent upward trend and the long-term rate has had a more volatile journey. In some cases, when the Fed has increased the short-term rate, the long-term rate has gone down! My point in all of this is to illustrate that what the media reports is not always about mortgage rates and that it is important to stay connected to accurate data.

Matthew Gardner, Windermere’s Chief Economist recently recorded a video update featured below that speaks to some of the misconceptions about interest rates, specifically mortgage rates. Many consumers are confused and misinformed which is dangerous. Investing in real estate is the single largest wealth-building opportunity and to not be accurately connected to the latest trends could get in the way of a successful financial picture.

Prices in many markets have already bottomed out from the 2022 correction and mortgage rates have come down off the peak. In some areas, we are already seeing appreciation again! This quote from Matthew sums up where we are headed. “Myself, and every economist I know, believe that rates will slowly pull back as we move through 2023, and I haven’t seen a single forecast suggesting that mortgage rates will rise to a level this country hasn’t seen in decades”.

With inflation slowing and year-over-year CPI (Consumer Price Index) numbers becoming less extreme, mortgage rates will start to soften. In fact, there are some important reports coming up in May that will tell this story. Real estate is a long-term hold investment that has been the cornerstone of wealth in our country. The wave we have had to ride post-pandemic related to supply chain issues and consumer demand is coming to the shore and real estate will remain an investment safe haven.

Another point to consider is while real estate is an investment is it also where you live. Life changes, good or bad, lead to moves. All this to say, remain nimble by being well-informed. Knowledge empowers strong decisions and accuracy matters. You can count on me to provide you with the information you need to successfully navigate your real estate decisions. Please reach out if you’d like to discuss how the current trends relate to your goals.

Shred Day & Food Drive was a huge success!

Big thank you to everyone who came by to utilize our free shredding services and drop off food or cash donations for the Volunteers of America Western Washington food banks!

We filled two trucks of shredding and collected over 2,000 pounds of food and $3,372 which will go to our neighbors in need. Thank you for your generosity!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

Since 1984, Windermere associates have dedicated a day of work to complete neighborhood improvement projects as part of Windermere’s Community Service Day. After all, real estate is rooted in our communities. And an investment in our neighborhoods gives us all a better place to call home.

Our office will spend the day with the Snohomish Garden Club working to put fresh produce on the tables of local families who need a little help. We will plant over a half-acre of veggies and fruits that will be harvested over the summer and into the fall.

If you’d like to pitch in, we are looking for additional veggie starts. Let me know if you have some starts already going or if you would like to prepare some now that you would be willing to donate. Our planting day is Friday, June 9th; I can arrange the details with you for drop off or pick up!

The garden specifically needs:

- Scallions

- Snow/Pod Peas (please no shelling peas)

- Chard

- Lettuce (the food banks require headed varieties, rather than loose-leaf)

- Squash (any kind, EXCEPT yellow crookneck)

- Cabbage/Broccoli/Kohlrabi/Cauliflower/Collards/Kale

- Peppers (early maturing varieties work great: ~70-day range)

- Herbs (never enough Basil and Parsley!)

- Flowers (marigolds, nasturtiums, or any annuals)